An equity crowdfunding campaign should be an early seed staging post on every start-up journey.

For Ebru Evrim, fresh off the pandemic and looking to leverage the first small studio in Skipton for a much bigger one in Harrogate to take advantage of a changing high street, it was always going to be a tough sell. New branches of anything cost a lot of money to restore and establish, however it’s done.

Despite the degree of difficulty, Seedrs encouraged the corporate structure, pitch deck and campaign momentum that helped procure £200k in EIS equity, £300k in convertible loan notes, and a £75k 12 month interest only loan over the campaign period. So a total £575k between launching the campaign and closing it cost £2,500 in campaign fees.

Thank you Laura and Seedrs, you are every seed stage start up’s dream!

That under the belt, attention switched to Leeds, to add a city branch to small town Skipton and big town Harrogate. A Leeds branch would complete the brand concept on a scaleable platform, in a way that would deliver founder, management and investors clear data on where to expand from there.

As luck would have it, Rushbond PLC were looking for a dynamic tenant for First White Cloth Hall, an historic listed building they had restored with the help of Historic England and the The National Lottery Heritage Fund, in a combined effort to rejuvenate Kirkgate, the oldest street in Leeds city center.

The restoration was tailor made for an Ebru Evrim branch, and located in the right area to draw on the different income streams that make up the brand. While Kirkgate was never going to become another James St in Harrogate, it had the potential to develop in a direction that we thought we could play an early part in, and benefit from.

With Harrogate and Skipton cash positive now, we are looking for equity investment upfront for Leeds, off a Polymath pitch deck template, which is original freestyle like everything Polymath branded, and I hope sufficient to spark the interest of an investment fund who likes the look of the sapling.

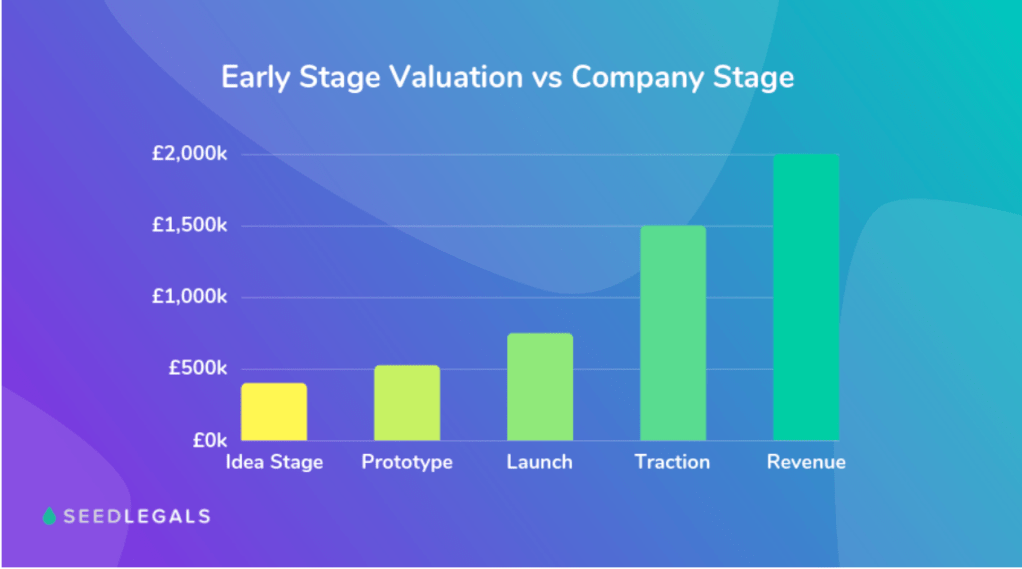

Anyone looking to go big who hasn’t been on a crowd equity funding campaign page before might find some of the pre-money cap valuations a little frothy. Mature company value indicators like P/E ratios don’t make much sense at the early stage, which would be anywhere from back of an envelope on the kitchen table, to revenue generating prototype on the high street. The first thing the £100k big blind looking to join the Ebru Evrim cap table needs to know is where the game is at, before they settle into their seat, and order the same punchy cocktail as the £50k small blind.

Seedrs £1.8m Ebru Evrim Ltd cap value supported by SeedLegals cap value locator guidelines

Start-ups come in all shapes and sizes, and each case has a past, present and future that must be judged on merits, but generally speaking platforms like Seedrs are there to help start-up entrepreneurs raise much needed growth capital without giving away all their shares at the beginning. While Dragon’s Den makes for good viewing, and netting a Dragon has it’s own intrinsic value (and dangers), in the real world at seed investment stage, no one expects entrepreneurs who’ve put heart, soul, £50k savings and their house on the line to give away much more than 20% to get to where they’re aiming for, unless they’re a Silicon Valley start-up with a billion dollar Unicorn in their pocket.

So where does the entrepreneur start, once the business has a growth aim that requires outside investment, and crowd equity funding is a suitable option? They can work out how much investment their plan needs, and go forward from there, then decide how much equity to give away, and work backwards from there. Somewhere in the middle, a sum of money gets attached to a % of shares that can be justified by other measures, like past and projected turnover, gross margins, intangibles like brand concept, customer data, business strategy, the team, and other points of difference highlighted in the campaign pitch deck, a pdf power point style presentation that must meet the approval of the crowd equity funding platform experts from the outset, long before the campaign goes live.

The Pitch Deck

The pitch deck will help determine where the start-up is in it’s early development cycle, and with one scaleable branch prototype trading, and another in the pipeline, Ebru Evrim has good traction and proven revenue streams that put the brand firmly in the revenue column valuation stage, which would, with supporting metrics and measures, cover valuations up to £2m, broadly speaking.

Pitch deck headings index

Those building blocks are summarised in the Ebru Evrim pitch deck presentation, which can be requested off the Seedrs campaign page menu under Documents. That’s the full picture in a user friendly format that supports a £1.8m cap valuation, when taken in the context of the extended investor offer on the campaign page, which is 10% of the brand for £200k minimum target to fit-out Harrogate branch, up to a stretch target of £550k for 27.5% to take the brand to a three branch membership triangle of small-town Skipton, big-town Harrogate, small-city Leeds, in one raise.

One £550k visit to the Seedrs platform is the preferred option, not so much because preparing for and working on a raise is tough and time-consuming, and so better all done at once, but more to make sure the brand is ready to move on a Leeds premises in mid-2022, after Harrogate is open, when the best options should be available, to open mid-2023, when Leeds city footfall is recovering in a new environment with new brands able to afford rent at new, reduced levels.

Supporting Documents

The Ebru Evrim campaign page and the pitch deck presentation are not the only measures available to investors. Those who want to dig deeper can engage with Ebru Evrim Ltd company directors, to acquire accounts for 2019 / 2020 and 2020 / 2021 prepared by Matthew Hindle at established accountants Wheawill and Sudworth, and detailed three year cashflow sheets, profit and loss projections and balance sheet prepared by brand development agency Polymath Creations’ Jonathan Roberts (also Ebru Evrim Director). They can also access Tom Kenyon Slaney, Founder and Chairman of the largest speaker agency in Europe and Asia the London Speaker Bureau, and an experienced Angel investor, for his extended take on the brand, and its prospects.

Committed start-up investors, diligent professionals and hands on multi-taskers help deliver campaign plans

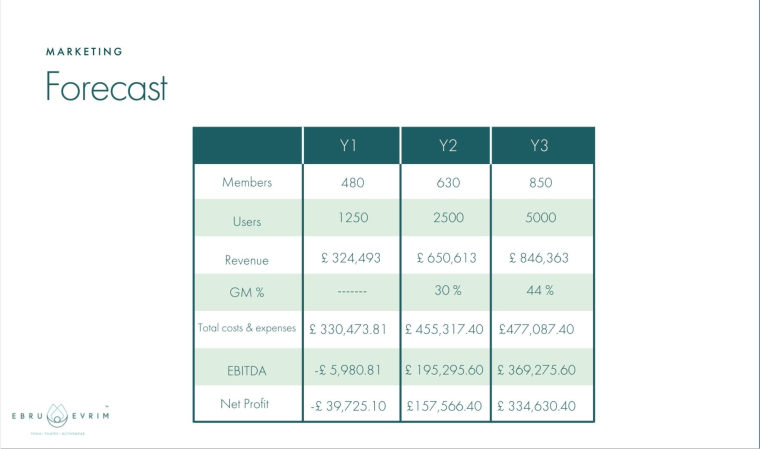

Taking a successful Seedrs campaign that overshoots the £200k minimum target by 50% to raise £300k for 15% equity that covers Harrogate branch, bespoke software, and the option of new Yoga studio in Skipton, prepared accounts from Jan 2019 to Jan 2021 and management accounts tracking performance from Jan 2021 to end Dec 2021 were the baseline for three year cashflow sheet and P&L projections with income stream assumptions including membership data from covid-affected Skipton, while excluding Harrogate communal area cafe figures for which there is no previous data to work off. Those figures and the membership numbers behind the extrapolations are part of the pitch deck.

Bottom line financial forecast

Spend Per Head

The marketing forecast table suggests membership spend per head of under £1,000, if an allowance is made for revenue from ‘users’, who are customers, but not members. But looking at future spend per head growth potential off an existing covid-affected spending pattern baseline, those projections look quite conservative.

If we take an average spend per head across all membership categories of £500 a year (Gold £59.99 p/m, Silver £39.99) that would be the direct debit revenue base for the other Ebru Evrim cross-selling income streams. Those would include an average £300 per member for activewear and equipment priced between £12.99 for toe socks to £74.99 for the latest leggings, and another £500 for workshops, retreats and wellness holidays that range in price from £35 to £2,000, which all together should even out to a £1,300 spend per member head off currently proven income streams with two branches up and running. As yet unproven figures from plans to use the extra ground floor space in Harrogate and future branches to add a healthy living cafe to the communal area and income from teacher training would be likely to lift that to above £1,500.

Healthy Living Cafe in communal area planned for Harrogate branch on

Detailed notes that accompany the cashflow sheets cover membership number projections built off the Skipton branch in more detail, but anticipated membership spend per head averages are a quick way to cross-reference and double check the veracity of those forecasts.

It’s also a good metric to support the £1.8m pre-money cap valuation. With projected spend per head growth potential from where the brand is now taken into account, a £1.8m cap valuation that might look at first glance on the high side, especially to investors not accustomed to seed investment stage valuations, is on closer inspection a destination driven valuation from a stable departure point that reflects proven value in the combination of Yoga and Pilates studios under one roof, a membership-based business model suitable for branch expansion, and existing and planned mixed income streams that contribute to a high spend per member. Growing on-line sales to the wider world, particularly activewear through an Ebru Evrim store, is the internet icing on the high street studio cake.

Ebru Evrim campaign page on Seedrs platform with the Little Blind at the table

So while a £200k minimum campaign raise for 10% of the brand off a £1.8m cap valuation is to a certain extent a means towards an end, and that end is a new branch that once up and running represents significant barriers to entry that help remove a large % of start-up failure risk, a £100k big blind pour encourager les autres unlocks another level of possibility – momentum towards a £550k stretch raise that Polymath Creations project management can turn into the Skipton Harrogate Leeds branch triangle that generates revenue for an organic one a year branch expansion plan, or alternatively a sound base for a decent exit.

Golden Triangles

What might that Skipton Harrogate Leeds golden triangle look like, based on gross margin average income streams, including membership, at 50%, a combined membership of 1,500, and an average spend per head of £1,500? A £2.25m turnover at a gross margin of 50% is EBITDA of £1.125m, after 20% VAT and 25% corporation tax and £30k annual loan / lease interest payment, not far off £600k. That is £300k for another branch and a £300k shareholders dividend, but £600k divided amongst 250,000 shares (which includes 35,000 convertible loan shares converted and 55,000 stretch raise shares for £550k that equity funds the golden triangle) is £2.40 earnings per share, and a P/E ratio of 4.2, at the current £10 share price. That platform would allow for a raise of £1.5m for 50,000 shares at £30 per share, off a £9m cap valuation at a 12.5 P/E ratio, to fund York and Manchester triangles, if equity driven growth was preferred to organic growth, into prime properties with Harrogate premises specifications, with projected turnover of £6.75m, and net profit of £1.8m.

Is that all? Not quite, especially if you’re an investor who pays higher rate income tax, and the start-up is qualified to sell Enterprise Investment Scheme (EIS) shares, like Ebru Evrim Ltd. Then, a £100k big blind investment into EIS shares would represent £37k at risk capital, and on the upside if things go to plan, a capital gains tax free exit after three years, and inheritance tax free transfer option after two years. A Polymath Post blog goes into more detail here.

Runways

And that’s that, apart from runways. Venture capitalists like to talk about runways, and that’s the capital and time required to get trading, and after covid they might talk about the extra power needed to climb up to the safe altitudes of break even, from take-off. The four month Skipton branch development and brand prototype creation runway with a Nov 2019 post-opening take-off climb saw membership grow to 130 in three months, with a lockdown affected aftermath described in more detail here, for anyone that’s interested.

Where would the brand be now, if there hadn’t been post covid lockdowns, which, like quantitative easing post sub-prime, were questionable policy responses to not unexpected cyclical events that had never been seen, or tried before?

That’s impossible to say. Artful low level piloting across a new landscape that household names like Laura Ashley couldn’t navigate, offered up a gilt edged opportunity to get in amongst big brands in a prime high street location at reduced rent. A six month Harrogate branch development plan, from signing the lease, through fit-out, to May 2022 opening, with a shopfront showroom and a Skipton branch growing steadily in the background as things get back to normal, and trading on or near break even most months, means little, if any, Seedrs investment will be burnt up on the Harrogate runway.

And with the 2020’s force majeure out of the way early doors, small adjustments to living standards from higher taxes and energy bills that won’t directly affect the Ebru Evrim customer and member demographic shouldn’t much affect flight paths for the rest of the decade.

But leaving preferred venture capital analogies and returning to this Polymath Post poker one, what the Polymath Creations croupier won’t have is the big blind, or the little blind, or anyone else at the Ebru Evrim cap table, including the Seedrs nominee, investing blind. Everyone gets dealt the same cards – from campaign page, to pitch deck, to prepared accounts and projected figures – as and when they request them. With a little delay sometimes, if it’s all hands on deck that week.

Bricks And Mortar

For those with extra curiosity, there is a Skipton branch class to attend, a new activewear range for sale in the Harrogate shopfront showroom to try, and, while the fit-out is ongoing, hard hat guided tours for those who like building sites and a bit of builder banter. But the virtual tour starts below.

Sign up and take your seat at the Ebru Evrim table as the big blind, or bet behind the Seedrs nominee!

In a highly regulated world, most law-abiding citizens who’ve made enough to become investors in start-ups don’t get to feel the buzz of evading tax and authority like the average money launderer, without risking a stretch at her Majesty’s leisure.

And then one day, presumably feeling sorry for their honest vassals who filled the coffers, Her Majesty’s Revenue & Customs (HMRC) gave birth to the Enterprise Investment Scheme (EIS), and, not long after, her smaller but slightly more attractive sister, the Seed Enterprise Investment Scheme (SEIS), and life for start-ups and investors changed forever.

Now, qualifying taxpayers could invest in qualifying start-ups, and offset the sum invested against income tax bills, and feel the buzz of evading tax like your average money launderer, with the full approval and encouragement of authority, and run only the risk that they’d lose their money, rather than their freedom, if the start-up went bust.

How exactly?

Let’s take a higher rate taxpayer, and a start-up that has received advance HMRC assurance it qualifies to receive SEIS investment. Each taxpayer is allowed to invest up to £100k in the start-up in any one year, which is in turn allowed to issue SEIS shares worth up to £150k total. Let’s say the investor buys £10k of shares in the start-up. Up to 50% of that (dependent on tax rate) can be offset against current or the previous year’s tax bill, which is a saving of up to £5k. If it were to be claimed against the previous year’s tax, HMRC send you a check in the post. Let’s not overlook the mental health benefits of this simple act of mercy on overburdened taxpayers.

And when SEIS runs out, what next?

Well, that’s when the EIS big sister gets involved. Each taxpayer is allowed to invest up to £1m EIS in what is now a company if it has survived, and the company is allowed to take up to £12m EIS investment over the course of its lifetime (£5m per year). But for EIS, only up to 30% of investment can be offset against income tax.

What’s the catch?

The investor has to hold the shares in the company for three years, and the company cannot begin with assets of over £200k, and must be a genuine start-up risk. So no ducking out early doors for investors, or asset prior purchases by start-ups which remove investment risk. Some of the rules of the game are clearer than others, but where HMRC is concerned, better to err on the side of caution where any doubt exists.

Any further incentives?

There are, actually. First, if an investor realises chargeable capital gains when selling an asset, payments to HMRC due on those gains can be deferred in proportion to the amount invested in a qualifying start-up or company. Secondly, once the SEIS / EIS shares have been held for 3 years, they can be sold capital gains tax free. And last but not least, once they have been held for 2 years, they can be passed on with 100% inheritance tax relief, making SEIS / EIS shares an important, if little know, potential part of estate planning. This is what makes the money launderers jealous. Investor’s who pick a winner can sell these shares without paying another penny in tax, and that, in a climate where everyone knows capital gains tax can only go up, might mean substantial savings at some future date.

And if the start-up or company goes bust?

Investors can claim loss relief, which when added to investment relief already claimed, means effectively that in the worse-case scenario, for EIS a 45% rate taxpayer shouldn’t be exposed to more than 38.5p loss in every £, for SEIS that’s down to 27.5p, because the rest would have ended up in HMRC’s coffers anyway if the taxpayer preferred to pay the taxman direct. In that instance, none of the SEIS / EIS capital gains and inheritance tax advantages count, of course. No risk, no reward, a dictum that every investor and entrepreneur uninfected by subsidies understands and loves, or they’d prefer boring old government bonds, or gold.

Drilling Down On Detail

Tax BreakingConclusion

When all is said and done, this is a brilliant scheme, and one that benefits investors, entrepreneurs, and the taxman, which is why one can confidently predict it will survive changing governments, and most other things, up to Armageddon. But, just like the Reformer, the awesome Pilates bed of springs invented by Jospeh Pilates nearly 100 years ago with the potential to transform lives, it takes time for word to get out, especially beyond seasoned circles.

Renaldo on Pilates Reformer

Crowd Equity Funding

But the investment landscape is changing, like the health landscape, and just like there are state-of-the-art studios like Ebru Evrim bringing clients and Pilates Reformers together to change physical health, there are investment platforms like Seedrs bringing an ever widening circle of investors and startups together, in ways that can change financial health, if approached with the right attitude.

Who Are Seedrs?

You can think of them as the London Stock Exchange of the UK / EU start-up universe, an FCA regulated blue chip crowd equity funding platform, doing the same job for start-ups that the famous exchanges do for public listed companies. They recently teamed up with Republic, a US crowd equity funding platform, offering the same service to start-ups looking to grow in the American market, which is regulated by the FSA. Seedrs were one of the first crowd equity funding platforms, founded in 2012.

Where do I start?

As always, when it comes to something new, the best way to learn about it is to have a go. Start-ups like Ebru Evrim Ltd go through a comprehensive vetting process when they put themselves forward to raise equity investment through Seedrs, including fact checking for every statement made on the Seedrs campaign platform. They are the experts at helping what are often frenetic startups working long hours to gain traction in their sector take that next step, with professional shareholder agreements that dovetail into standard articles of association, and a subscription agreement that secures Seedrs nominee shareholders, and by implication, any other shareholders.

And when finance is tight, as it is for most in the early start-up phase, the level of expertise they bring to the table is fantastic value for money, with almost all payment taken after the raise, and then only if the campaign is a success and the minimum target is reached. That leaves start-up founder entrepreneur(s) and team with the extra time and resource to build the brand out into the marketplace, to the point where the business is big enough and revenue is strong enough to pay for specialists and experts who can share some of the strain of a growing business for some of the gain.

What does all this mean for investors?

It means that any qualified SEIS / EIS startup, or early stage company, that appears on the Seedrs platform, has passed HMRC advance assurance to sell SEIS / EIS shares, and has passed Seedrs due diligence, so will say what it does on the tin by the time the campaign goes live on the Seedrs platform, first to the start-up’s own community through Priority Access (below), and then through Public Access to the wider Seedrs investment community. To sign-up to the platform, investors need to prove they understand risk reward, by answering a few simple questions, and then before they invest, go through a verification process which, sadly for the money launderers, includes basic ID document and proof of address checks. So this is a legal buzz they’ll have to miss out on.

Buy EIS Shares in Ebru Evrim Ltd At Seedrs

Click here or above image for Priority Access at ebruevrim.com

For those who want to put a £10 toe into the SEIS / EIS water, or take a £100k deep dive, the Seedrs platform is a great place to start.

Yoga & Pilates Studios Under One Roof

Sounds so obvious, you wonder why no one thought of it before.

It’s The Company You Keep

Two doors down Russell & Bromley, four doors down Apple, to the high street born @ http://ebruevrim.com

Disclaimer

Investing involves risks, including loss of capital, illiquidity, lack of dividends and dilution, and should be done only as part of a diversified portfolio. Please read the Risk Warnings before investing. Investments should only be made by investors who understand these risks. Tax treatment depends on individual circumstances and is subject to change in future. Seedrs does not make investment recommendations to you and any investment decision should be made on the basis of the full campaign. No communications from Seedrs, through email or any other medium, should be construed as an investment recommendation.

This blog post has been approved as a financial promotion by Seedrs Limited.

Seedrs Limited is authorised and regulated by the Financial Conduct Authority. Seedrs Limited is a limited company, registered in England and Wales (No. 06848016), with registered office at Churchill House, 142-146 Old Street, London EC1V 9BW.

A plane is at its most vulnerable just after take-off, when there’s no altitude to react to any malfunction, mistake or external hazard, and it’s the same for brands. As a passenger, it makes much more sense to grip your seat as you power off the tarmac, rather than during turbulence at 30,000 feet, or when you are coming in to land. As a pilot, or the owner of a brand that has just launched, your first focus is getting completely airborne with happy customers and decent revenues in the first trading quarter. More often than not, this revenue will be what pays off outstanding supplier invoices.

That was the case with Ebru Evrim, a state of the art Yoga and Pilates studio in the market town of Skipton, which took six months to design and renovate, at a cost close to £250k. Working on an old building is a bit like working on an archeological dig; until you start excavations, you don’t know what you’ll find, and what you find will to a certain extent determine what you can do to transform the space.

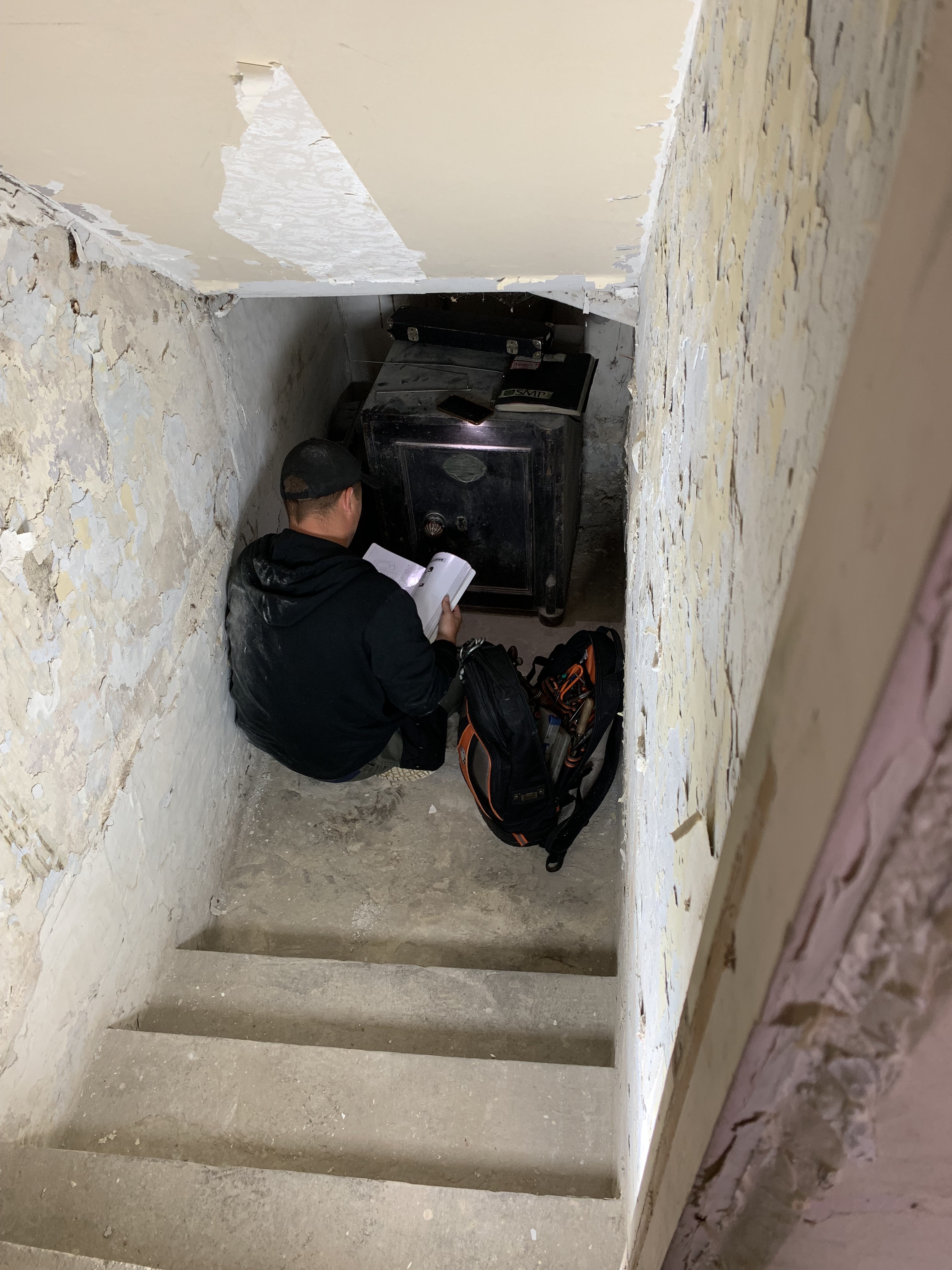

A safecracker called in to investigate the discovery of a locked antique safe hidden away beneath a false floor removed to check if the stairs beneath led to a cellar. As onlookers’ imaginations ran wild, the door swung open to reveal ….. a dusty HMRC VAT return form from the 1960’s. A stark reminder that this was a cellar in Skipton, Gateway to the Yorkshire Dales, populated by thrifty Yorkshire folk with a wicked sense of humour, not some hidden crypt in Luxor, Valley of the Kings in an Indiana Jones movie.

As plaster was removed to expose original building stone, and ceilings ripped out to reveal a massive 250 year old oak Queen truss roof beam, the plan to develop a prototype studio concept that could be scaled into other market towns was changed to develop a prototype boutique studio concept that would scale into other market towns, and in that one word is a doubling or tripling of budgets, because once you see boutique, it’s in for a penny, in for a pound, your aim is a product that won’t find like for like competitors moving in just up the high street to take a share of your customer cake for themselves!

And it’s not just the extra investment required to deliver the unique boutique design and atmosphere, it’s extra time. Some of the effort, especially the cleaning up of the stone, is slow, artisanal work that can’t be knocked off quickly to a tight deadline. And once you’re into a natural stone look, you’re into natural wood and glass to complement it. The old pine floorboards were replaced by a modern oak floor with underfloor heating, but the wood wasn’t thrown away, old cut floor brad nails were removed by hand, and the wood recycled into doors, shelving and furniture by a local cabinet maker.

Doing a boutique restoration is a state of mind where the design concept is carefully worked into the structure’s existing fabric, and then furniture and equipment with the right look and feel is sourced as it becomes clear what will fit in best. At the same time, things are moving fast, and without focus and foresight, some aesthetic possibility that must be seen and planned for in advance to fit in with building schedules, might have to be ignored. It’s like playing heads up rugby in broken play. Is there any area of life that doesn’t reward spatial awareness?

The other calculation that can’t be taught in text books, as the bills mount and deadlines pass into the rear view mirror, is how much projected trading income lost in delays caused by going boutique can be justified by value added to the brand when creating a unique design concept that can’t be copied, and the customer loyalty that accrues from that. We went the extra mile at every turn because there are a lot of functional branches of gym chains out there, even in market towns like Skipton, often with a studio space for classes, with a vibe tailored towards gym enthusiasts that doesn’t always sit well with the Yoga and Pilates crowd. And the alternatives are mostly public places for hire or rooms turned into studios which lack atmosphere and a level of service that can only come from a level of organisation that adds significantly to overheads. Nailing boutique means higher entry barriers for new arrivals, so most startups looking to secure a unique prototype look for that, but what’s not so easy to find is the extra money to fund it on the hoof, while building works are ongoing.

Ebru Evrim opened on Nov 24th, a date set in stone a month earlier to accommodate a free opening day of classes and a drinks party at Ellsworth Restaurant in the evening. That was the last weekend before everyone begins to focus in Christmas, and the latest the studio could open without stepping into dangerous cashflow territory. The state of the art Pilates equipment arrived a week later after last minute tax and shipping complications, and the activewear window display was only full because the Polymath bagman flew over to Istanbul to pick up a suitcase full of stock the day before opening. Some of those issues were related to the extra cost of going boutique, and in the end the first activewear range order only arrived in its entirety three months later, which turned out to be just before the pandemic struck.

Luckily by then the Ebru Evrim brand was fully airborne, with 130 happy passengers on board. At the planning stage it had been calculated that a full class timetable for Yoga and Pilates could handle 350 members, that that was in effect a full plane, and we’d allowed three years to get to that point. By the end of February, a month or so before the first lockdown and the full extent of what Covid would mean began to materialise, it looked like full member capacity would arrive at the end of the first year, or even sooner. Happy days! An even more important three month target – break even where monthly income exceeded monthly costs – was around 120 members. By the end of the first free months it was evident from the positive feedback that boutique had been worth the effort, despite the extra burden that placed on restoration budgets and opening deadlines.

At that stage the brand launch from kitchen table to high street opening had been about 80% paid for by a balance of equity, convertible loans and asset finance. The outstanding 15% owing was mostly final payments to suppliers, who agreed to monthly installments, since despite the excellent start, and the promise that a Founder’s investment would be matched by a startup loan, Barclay’s Bank wasn’t prepared to divvy up. Every other source of investment, inevitably friends and family at this early stage when it’s easy to doubt a brand will ever make it onto the high street, had gone the extra mile that came with going boutique, but the bank weren’t even prepared to do what they said they’d do on the tin. Luckily the firms involved were big enough to absorb the delay to final payment.

The only potential source of finance identified early on more risk averse and less understanding than Barclays was the State’s very own Business Enterprise Fund (BEF) who used the activewear as an excuse to duck their responsibility, despite that being the icing on the cake, the extra income earner that would complete the brand mix, not determine the fundamental viability that would cover the cost of their State secured loan. And their choice fulfilled their own prophecy, since that investment would have bought an online sales and marketing campaign, without which activewear sales growth would have to build towards requisite online marketing budgets from in studio sales. There is a very clear return on advertising (ROA) correlation between online advertising and sales, where the ROA climbs as early advertising within the correct online setup is steadily increased. There’s no real shortcut to that, other than a friendly celeb with a multimillion insta following who pushes your product for free.

As for Covid, for the Ebru Evrim brand, ever dark cloud has a sliver lining. The excellent first three months trading figures extrapolated to a year’s turnover resulted in a Bounce Back Loan from Barclays (that should have come a month earlier as a startup loan), which paid off the last remaining restoration bills, with a little left over to set up online classes. With online classes and the goodwill and loyalty of the members to the brand, membership cancellations were kept to a minimum. While it was impossible to give the activewear the online sales and marketing investment it needed, it was possible with the continued monthly membership income and by taking advantage of furlough and grants, to make it through all the stop start with just another £10k added to convertible loan stock. The brand could have bled out with monthly losses of anything more than £2k a month, sending £250k down the plughole.

Covid did force some painful management decisions to cut costs. Overall, the Studio Manager who’d done a great job supporting the Founder Owner in getting everything going, her assistant manager, and some of the freelance teachers, ended up being replaced by a more cost effective management structure with a Studio Manager who taught Pilates and Yoga to a very high standard, backed up by the Founder Owner, running a pared back class timetable switched online during lockdowns.

In relation to future branch expansion plans, the pandemic forced a change that improved management structure efficiency of the business model by creating a better and more cost effective balance between permanent and freelance teachers, and highlighted how flexible and resilient the business model was to upturns, downturns, and even closures, with Ebru Evrim able to increase or decrease the number of classes taught by freelance teachers as the market dictated. That way, the burden was borne more or less equally, and as soon as membership grows again, freelance teachers get hired to teach more classes.

It’s hard to imagine how much lockdown choices must have cost other startups, or indeed any business where even with government support, monthly losses were significant. As anyone who runs a business knows, what looks like a containable monthly loss soon adds up, even in normal trading conditions. Switch the income tap off completely, and just like being stranded in a desert without water, many perish. All that can be hoped, when all is said and done and independently audited (I’d recommend a Gocompare enquiry, since different approaches led to different results, and everyone wants to make the best choice next time with real data from this effort fully digested), is that honest calculations were made, and the cure doesn’t end up costing more than the disease.

No one crows about surviving a force majeure that kills off or disrupts competitors, even if that was a likely outcome anyway under normal market conditions; it’s more like relief mixed with commiseration. The reality for Ebru Evrim as things stand is that the pandemic accelerated changes and demographics that were already moving in the brand’s favour, which is why it was created in the first place. For example, a steady stream of new arrivals from big cities became a mini flood.

The lost year was an opportunity to tinker with the online platform for activewear, and improve online capabilities as far as possible, as a support to in studio classes. Were online classes massively popular? Yes, up to a point. So can we scrap the studio, and just invest in online growth, that of course received a boost in lockdown? Not according to our members, who found it hard to maintain class attendance discipline during lockdown, who missed the social aspect of the studio, and who can’t wait to get back to in studio classes. Rather, we are looking at ways to enlarge studio capacity.

From the first three months trading, it was clear where the brand was going without Covid. But survival of Black Swan events, where the business model is tested at the outset in ways that wouldn’t normally occur, where worse case scenario flexibility is taken to extremes, is perhaps in the long term a better way to get to a position of strength and safety, because so much more gets learnt along the way. That’s from the ‘if it doesn’t kill you, it makes you stronger’ Nietzschean school of thought.

There’s also the ‘beware the hero complex’ caveat that comes with big government decision making, where good intentions get kidnapped by political forces with ideologies that add to or even create problems so that attention seekers can solve them in a way that suits their agenda, while claiming saviour status. The brand wouldn’t have survived the lockdowns without government assistance, but it would have survived the pandemic without lockdowns. So we are entitled to opinions on pandemic policy, as wealth and job creators, and taxpayers.

Ebru Evrim is a small business, one of many, that prides itself on being self-reliant and independent. It is part of the private sector, which takes calculated risks to provide the energy and income that big government taxes to deliver services that society demand. Part solving a problem that you part created isn’t a good audition to handicap, blinker or even hood the horse of private enterprise, and then demand it races flat out against less burdened competitors on a tricky new course with artificial obstacles. After some rocky, ropey, dopey style Wuhan racing, most at the business end starting to feel the whip on their flanks want to know what the new race course looks like, and what those holding the reins swear by and now believe in, when racing on the old track by old rules was hard enough.

While it’s tough to do much more than speculate on forces that dominate the bigger command and control picture, Ebru Evrim has emerged from Covid in pole position to expand market share with a few improvements to the business model that the last year has identified, an opportunity that makes it worthwhile bringing on some new investors to raise the capital to speed that process up. The brand is perfectly positioned and prepared to take full advantage of a crowd equity funding platform like Seedrs, who offer a nominee shareholder service where they act as market makers for a raise typically targeting a larger pool of investors making lower average per capita investments, including Ebru Evrim members and followers, who can take an affordable stake in a business they know well.

While a well-appointed office at home might provide welcome relief from a grueling commute, or some working sanctuary from home life, why stop there? The selective use of an international home office, especially one in a different culture, can take your creativity and productivity off the charts. If you have the freedom to allot time and resource according to how it benefits your productivity, then get ahead of the work space revolution, and give a carefully chosen iHomeOffice in an inspiring location a decent run for its money.

In addition to using recyclable products like glass in the manufacturing process wherever possible, Opal Oceans will launch with a special edition Ocean Minerals cologne which will make a donation from every bottle to keeping the sea clean for our friends the dolphins, especially from Covid face masks and the Low Frequency Noise pollution of Coastal Wind Turbine farms which interfere with their unique communication frequency as much as they interfere with human and animal health and wellbeing on land. Out of sight may be out of mind for some profiteers, but not to our friends in the sea, or anybody who struggles to pay their electricity bill, and wonders what’s going on.

Creating a billion dollar brand like Coke Cola is as common as breeding and training a champion racehorse like Arkle. In fact, it’s hard enough to breed your own winner, never mind a champion. But, as the old cliche goes, it’s the journey that counts in life credits as much as the destination, so might as well give it a go.

BILLION DOLLAR BET

More often than not a farfetched or absurd aim is a sign that a previous realistic aim hasn’t been met. It’s easier to hide failure behind some unattainable dream than come to terms with and correct flaws that saw a more modest goal missed. My favorite current example in Sport is England Rugby Union coach Eddie Jones. After he lost the Rugby World Cup final because he stubbornly refused to accommodate a creative alternative to honest endeavor in the sport’s key creative position, his denial and then deflection came in the form of a new exhortation to his pet players, to be the best team the game has ever known. This ridiculous aim landed him and his pets a new contract, and supporters a boring brand of risk free rugby destined to lead back to the previous success levels at best. There’s no lack of self awareness to marvel at, what’s insulting to critical fans is the brazen contempt for their predictions, even after events proved them right. Who wants to hear that safety first certainty is the only option due to supposedly ingrained cultural shortcomings from the ugly boot and mouth of the oppressors who go out of their way to game, taunt, humiliate and destroy the viable creative alternative?

As in sport, that crucible of life, so in business. The chances of Opal Oceans, or Undercurrent Affairs becoming a billion dollar brand would seem remote. And nowhere in the sales blurb will you find such a preposterous claim. Technically it’s possible, there are examples of FMCG’s and new Media models developing into such big corporate beasts, more likely is slow burner to a million dollar turnover. But a blog called Billion Dollar Brand with the favourite Polymath runners featured has a much more alliterative roll to it than Million Dollar Brand, and the property gearing near miss in Istanbul that would have provided a more solid platform for take-off proved that the story behind any effort ground up on the frontiers is probably the ultimate way to add value to the brand. Turkish culture does a special kind of crazy, so Opal Oceans under mercurial leadership not afraid of failure is just as likely to end up a Billion Dollar Brand as any England team under Corporal Jones and the pugilistic Farrell is to end up Greatest Team Ever. Polymath Creations is working on it. We’re in it for the long haul

Then there’s Project Immortal. Adam Peaty is the greatest breastroke swimmer the world has ever know. Quite comfortably. He’s broken and holds all the world records at 50m and 100m, and needs to set himself new targets. So he, or his coaches, came up with the aim of the perfect swim, one so quick that it would never be beaten, and called it Project Immortal. To accomplish that, he’d have to swim the 50m in close to 55 seconds, a time that not long ago would have been considered impossible. Now it’s just unthinkable. Micro seconds is meters in a short sprint in the pool, and such a swim would leave competitors literally trailing in his wake. He wants to set a time that is so intimidating, rivals today and well into the future are beaten before they get into the pool. There’s nothing defensive or hopeful about that, or anything detached from reality. He is so far ahead of his rivals, he is effectively competing with himself. And in that case, he has the platform to attempt the unthinkable, and leave a record time that stands the test of time.

No doubt reconnaissance is seldom wasted, and should always be a multifaceted affair, but two years on foot under canvass in the Turkish Middle East leading a modest horse caravan as an emerging market entry strategy can’t help but be a multi-dimensional love affair with daytime spent looking down and nighttime looking up. Sadly, no records remain, so you’ll have to take my word for it, or do it yourself! I can reveal I had an excellent Russian guide called Ouspensky who I picked up in the UK before I left, and a set of exercises I stole off a Vietnamese buddhist called Thong in St John’s Wood London that helped me survive -30° nights and snowstorms over winter in Kars, which appropriately enough is Turkish for snow. I got off lightly enough, just a touch of PTSD that I bottled up with the rest of the experience, and stuck in the old cellar for minimum 20 years like instructed, come what may. Not long to opening time now!

The desolate Turkish North East in Kars district during winter, often compared with Siberia

The shift from fluid campaign to fixed organisation, if the opportunity arises, brings new challenges that it’s best to place in the context of longer term aims. Once the longer term aims have been identified, the correct organisation can be found to deliver them. For example, 25 years later, Save The Rhino, a not for profit, is still delivering on core aims established after an extensive African reconnaissance that fed into a successful Rhino Scramble campaign.

While most expeditions require plenty of preparation, a challenge can be quite private and spontaneous, and even reckless, like being dared by your mates to swim across the Thames in the dark after one too many at your local. The Douglas Challenge is a more calculated risk reward effort that sorts the men from the boys, a wild wetsuit free North Sea swim from the Bass Rock to Cliff View beach next to the Black Douglas seat of Tantallon Castle near North Berwick, to test hypothermia limits. If you can answer a question like ‘did you just swim from the Bass Rock’ through chattering teeth and frozen jaw, you’re still in your comfort zone!

Tantallon Castle, seat of the infamous Red Douglas clan, and the Bass RockThe landing zone at Seacliff beach, just under the Castle, at low tidestairway to 12 degreeshalf way house, bass rock and lighthouse arrière, sea gulls circling1hr 20 mins later, cold to the core, crowd build up at the finish line, home and hosed!